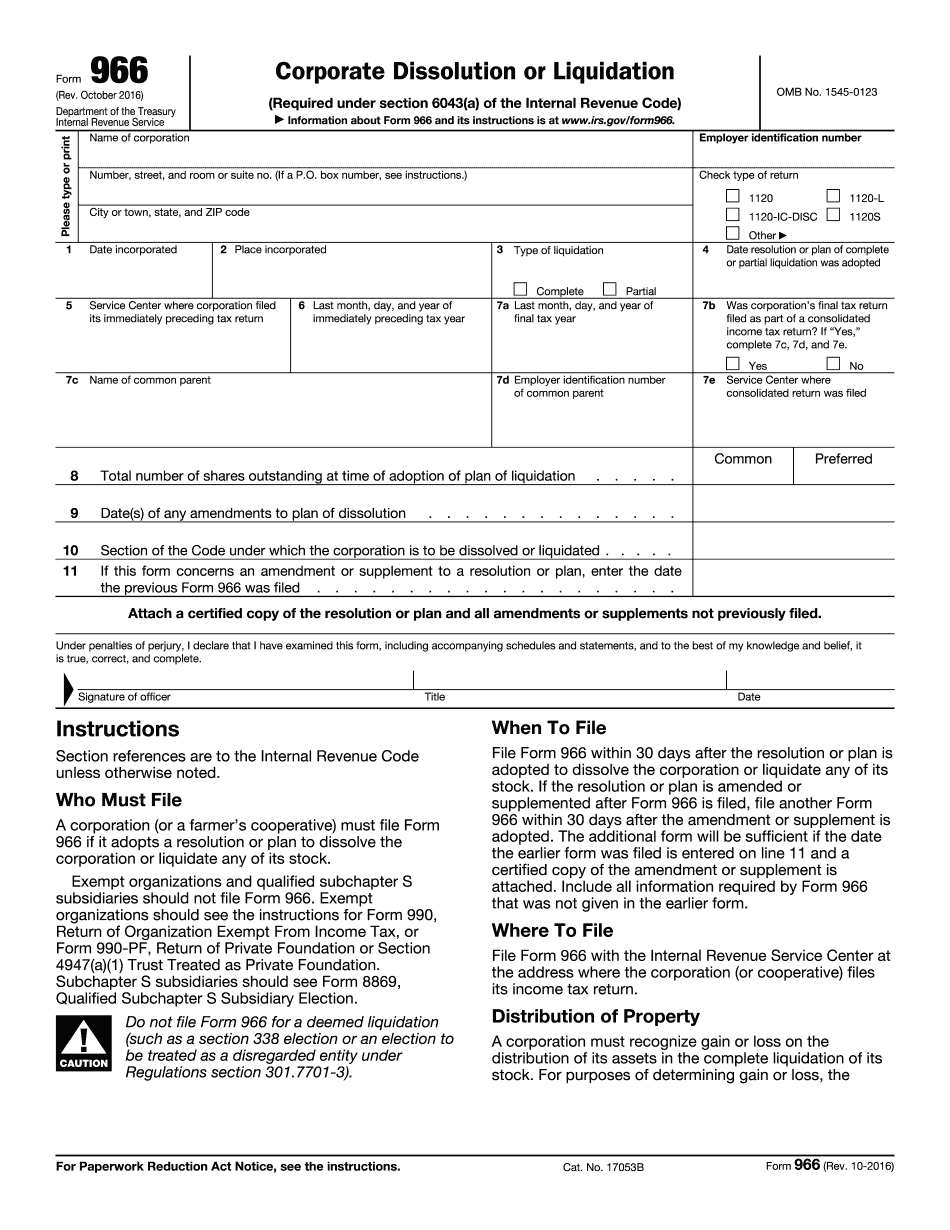

Hi class, we are now on chapter six which covers corporate liquidating distributions. In our last chapter, chapter four, we discussed non-liquidating distributions. In this case, we have a company that is going to distribute all of its assets and liabilities and pay off its debts, essentially liquidating. After liquidation, it may choose to shut down and dissolve as a corporate entity. This situation arises when management decides they no longer want to operate the corporation for various reasons. There are two ways to shut down a corporation. Firstly, you can sell all of the assets, pay taxes on the gain, and then distribute the cash from the sale, as well as any remaining cash, to shareholders. In this case, the corporation pays taxes on the gain from the asset sale, and the shareholders also pay taxes on the distribution. The distribution is treated as either a dividend or a return of basis, depending on the corporate E&P (Earnings & Profits). If the distribution exceeds the basis, it is treated as a capital gain. This first situation creates double taxation. The second way to shut down a corporation is by distributing the corporate assets to the shareholders. In this case, there are still two layers of tax on the gain, as we will see later in the book. There is a helpful example provided on page three, visually depicting the scenario. In the example, we have Randy Jones, the owner of Ball Corporation. Creditors are also involved, as well as an unrelated purchaser of some of April Corporation's assets. The government is shown as the receiver of taxes owed on the liquidation of the corporation. Randy is the hundred percent owner of April Corporation, which is a C corporation. Randy's basis in the stock is $100,000. The corporation's assets are as follows:...

Award-winning PDF software

Video instructions and help with filling out and completing What Is Irs Form 966