If you're creating any content online, whether it be a blog, podcast, video channel, or social media platform like Facebook, Twitter, or Instagram, it's important to have a well-crafted about or bio section. This is because many individuals rely on this section to determine whether or not they should continue following and consuming your content. In this video, we will discuss five essential factors to include in your about page in order to attract and retain followers and subscribers. If you haven't already done so, now is the perfect time to optimize your about page. Let's dive in! The first key element you need to include is an amazing hook. A hook is a compelling way to capture a person's attention right from the start, encouraging them to continue reading. Without a strong hook, the audience may leave and never return, regardless of the valuable content following it. There are several effective ways to hook your audience. One approach is to ask thought-provoking questions that resonate with your target audience. These questions should address their pain points and problems, eliciting a "yes, that's me" response. By understanding and addressing their concerns, they will likely continue exploring your about page. If you have adequate space on your website, another option for a great hook is to tell a captivating story. This story should be relatable and resonate with the reader, linking it to the pains and problems they may be experiencing. It's crucial to demonstrate your understanding of their situation. As marketing expert Jay Abraham suggests, if you can define the problem better than your target customer, they will assume you have the solution. Asking questions or telling a story that aligns with their experiences achieves this objective. However, it's important to strike a balance and not ramble on for too long. The...

Award-winning PDF software

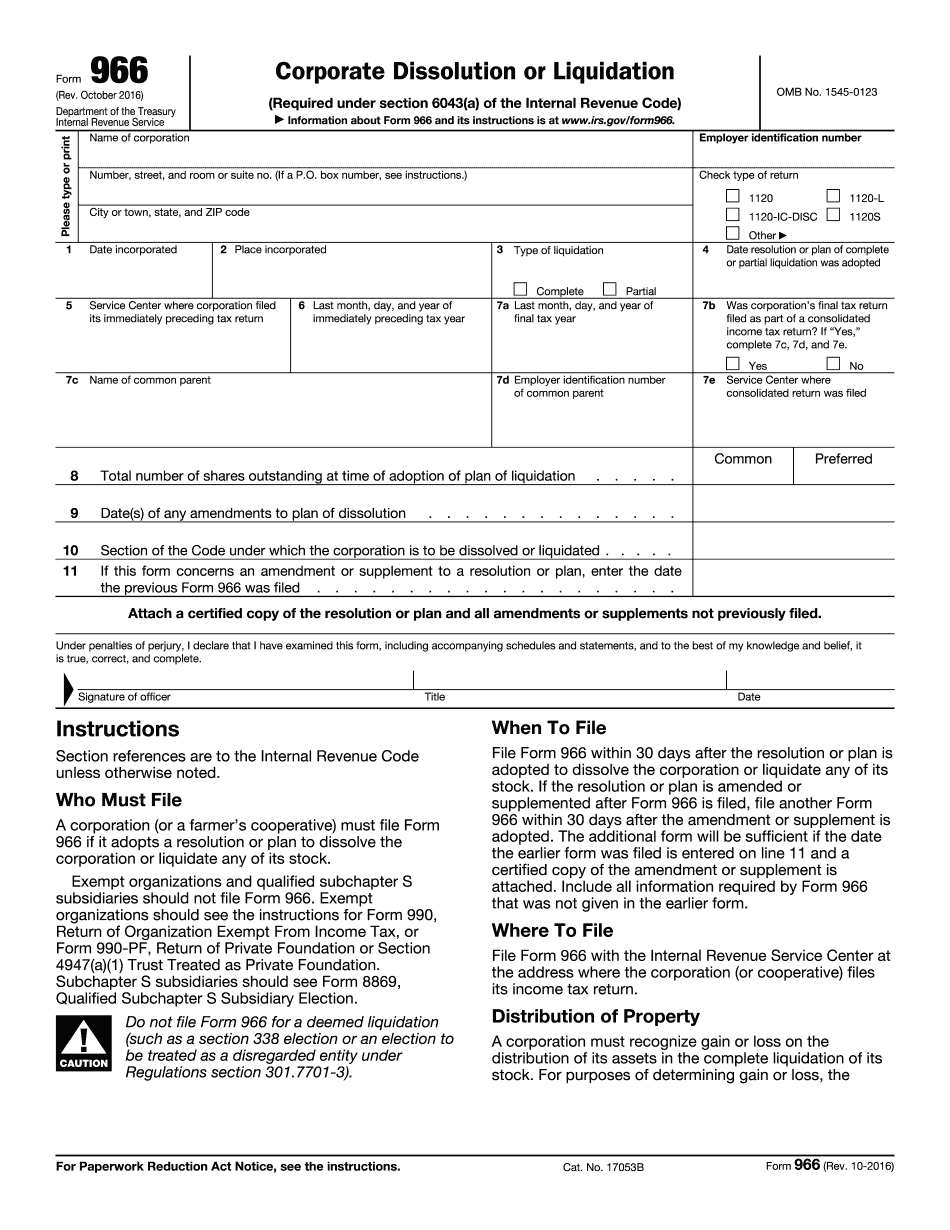

Section 6043(a) Form: What You Should Know

IRS-4434 and Temporary Regulations Implementing IRC Section 6043(a) (Liquidating, Etc., Transactions). The revised Form 990 is the one that takes effect with the final regulations, and the IRS has published two interim final rules under IRC Section 6043(g)(1) (liquidating, etc., Transactions) that require some corporations to submit additional information to the IRS for the purpose of determining the taxable status of a transaction in connection with a merger or acquisition. These rules are effective for taxable years ending after January 1, 2019. (b) Disclosure of transactions relating to a taxable merger or acquisition. (1) Final regulations. Under section 4940(j)(2) (transactions by a corporation other than an S corporation), the requirements of Section 6043(a)(2)(B) (liquidating, etc., Transaction) are to be applied. Section 4940(j) also provides that a partnership and its partners are to make a separate election under that section. Under IRC Section 6043(g)(5)(B) (transactions, (1), in connection with a merger or acquisition of a corporation, by and through the corporation or by or through its partners), the requirements of section 6043(a)(2)(B) are to be applied, except that a separate election by the partners that would defer the payment of the tax is not required. (2) Emergency regulation. The IRS may issue a temporary regulation authorizing a corporation not otherwise required to file a Form 990 to apply Section 4940(j)(2) with respect to the completion of an acquisition of property by a foreign person if there is a significant change in the nature or amount of the property (e.g., a significant shift in ownership of the interest of the corporation, in. which case the regulations would authorize the sale or other disposition of the property to satisfy the tax liability if the acquisition of the property by the foreign person is completed before the end of a period of five years after the date on which the corporation first Would have become subject to the tax if it had disposed of the property). Procedures in the event of a change of corporate Status. See also Rev. Pro. 2018-24, or, if the transferor is a foreign person or foreign partnership, section 6043. Sec. 6043. Liquidating, Etc.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 966, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 966 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 966 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 966 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Section 6043(a)