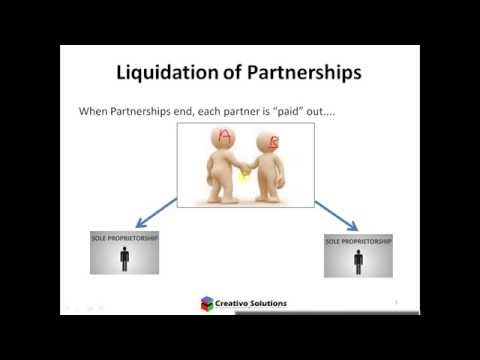

Hi everyone Anthony here from creativa solutions today I'm looking at financial accounting and we're focusing specifically on partnerships I've seen a lot of students struggle specifically with the peaceful liquidation so today I'm going to take you through the theory relating to partnerships and I'm then going to look through an example from start to finish showing you how to actually approach a peaceful liquidation question all right guys obviously creative solutions is here to help creatively add value to help find solutions so the video that you're currently watching is going to be covering the theory relating to partnership liquidations and then I'm going to form a separate piece for you which will take you through an example question show you the calculations and the steps to complete a peaceful liquidation so if you do want the question please go to the website WWWE be solutions calm down at the question and answer which will be posted there and also follow us on Twitter at creativa underscore s and stay tuned and watch our YouTube channel for any support content that will be released alright guys so to start off liquidation of partnerships do partnerships loss River no they don't hardships can end and if you've gone to the theory you'll remember that a partnership is not a separate legal entity so partners actually create the business partnerships let's say a and B okay there are two partners operating a partnership they are the business a and B are the business if one partner wants to leave this partnership has to be dissolved or if new partners had to come into the business then you'd also have to inverted commas dissolve the partnership and then create a new one right so in this particular video we're going to...

Award-winning PDF software

Corporate liquidation examples Form: What You Should Know

All corporation liquidations must be approved by the Governor in Council. The corporation must file this approval with the appropriate Minister of Finance Minister (as shown on their website) before commencing the liquidation. The Minister's address is: Federal Minister of Finance Ottawa, Ontario K1A 0D5 Attached to the application, you will find a notice of the application (the Notice of Application). The Notice must be served on the other shareholder(s), the board of directors and other authorized officers of the corporation. It must be served within 10 days from the commencement date of the liquidation. The notice of application must clearly state that you are the holder of the shares and of all the securities and obligations of the corporation, that the corporation no longer has or has the ability to exercise its powers and that you intend to make liquidation of the corporation. You must submit the required documentation to the liquidator who will prepare, at their discretion, a form (Form D) describing the assets and liabilities of the corporation and the liquidation plans. The liquidator will send you the appropriate information on the form to prepare this form, including a section dealing with the legal title (the “title”), and you must complete and file that section with the Minister of Finance in accordance with provincial rules. Provincial Laws Please note in the province you are filing for (or you intend to file for), you must first register with the provincial Department of Governmental Services (DGS). The DGS website is available here. Once registered, you can find out about the different filing, assessment and taxation requirements for corporations and for limited partnerships. You should submit your declaration of dissolution (Form 3014) to DGS no later than 60 days before the date of distribution (or the date the directors will be served with the notice of the proposed liquidation). DGS will provide you with contact information for provincial and federal officials to assist you with your filing. When you file, you must also indicate whether the corporation will be a limited partnership or a corporation (see below).

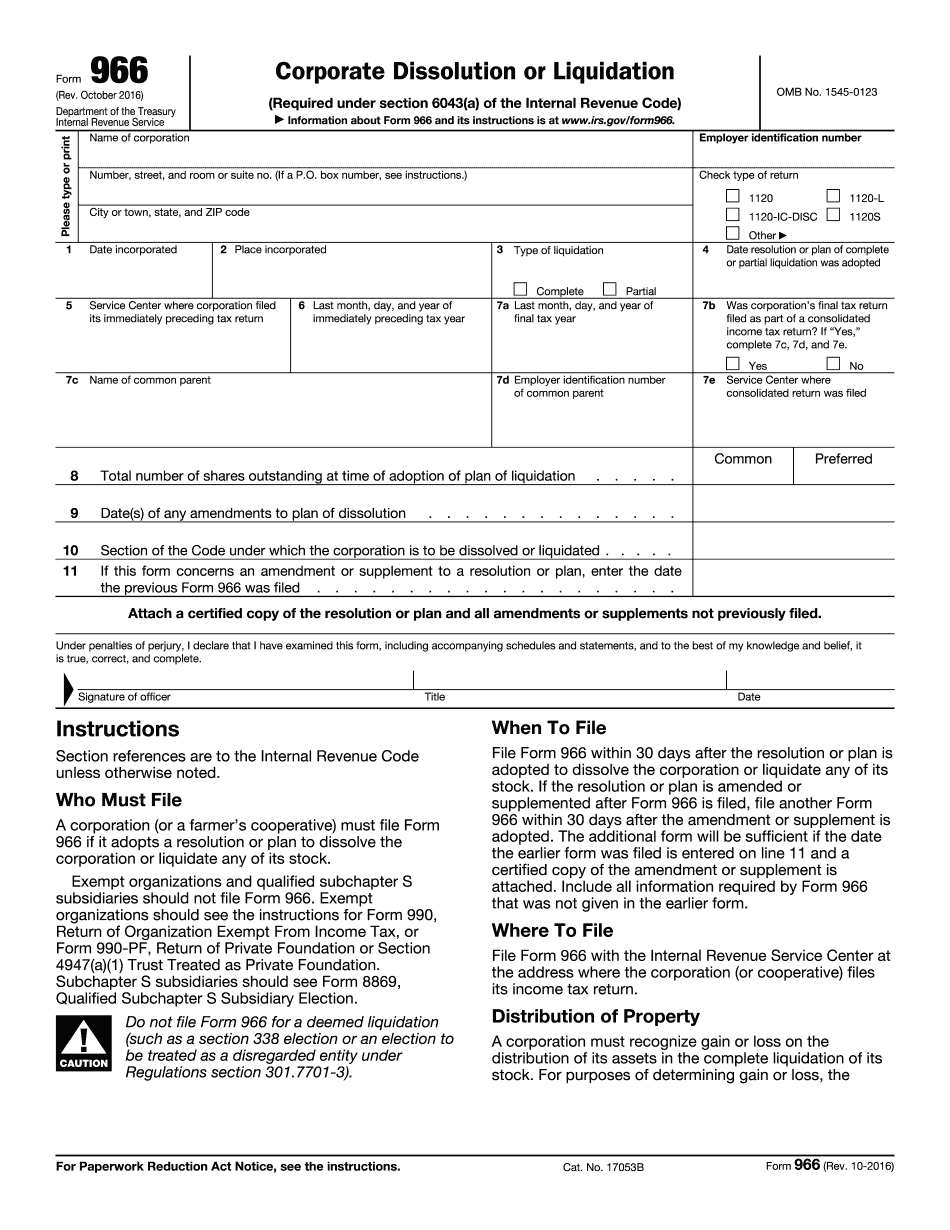

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 966, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 966 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 966 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 966 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Corporate liquidation examples