Shareholder basis for an S corporation is calculated similarly to a C corporation's basis. - The shareholder adds net income, separately stated items, and subtracts non-deductible expenses and distributions to their basis. - Shareholders of a liability partnership can add their share of liability to their basis, but S corporation shareholders cannot. - An exception is if a shareholder loans money to the company, they can add it to their basis. - However, guaranteeing a corporate loan does not increase a shareholder's basis. - Shareholders' stock basis can never be zero, it must be at least $1. - Partnership losses are only deductible up to the extent of a partner's outside basis. - If a partner receives a cash distribution exceeding their outside basis, the excess is taxed as a capital gain. - In regular corporations, basis in stock cannot fall below zero, only dividends reduce basis. - Liquidating dividends can reduce basis but not below zero, and any excess is taxed as capital gains. - In the case of a negative ending basis, ordering rules are needed. - In S corporations, the AAA account is distributed first, followed by existing accumulated earnings and profits. - The AAA account cannot go below zero due to distributions, but it can go below zero due to an NOL. - Any cash received goes against the shareholders' basis, and excess cash goes against capital gains. - In the presence of both distributions and net losses, distributions are taken before applying losses. - Net losses can only be taken to the extent of stock and loan basis, with the option to carry forward and deduct by the same shareholder.

Award-winning PDF software

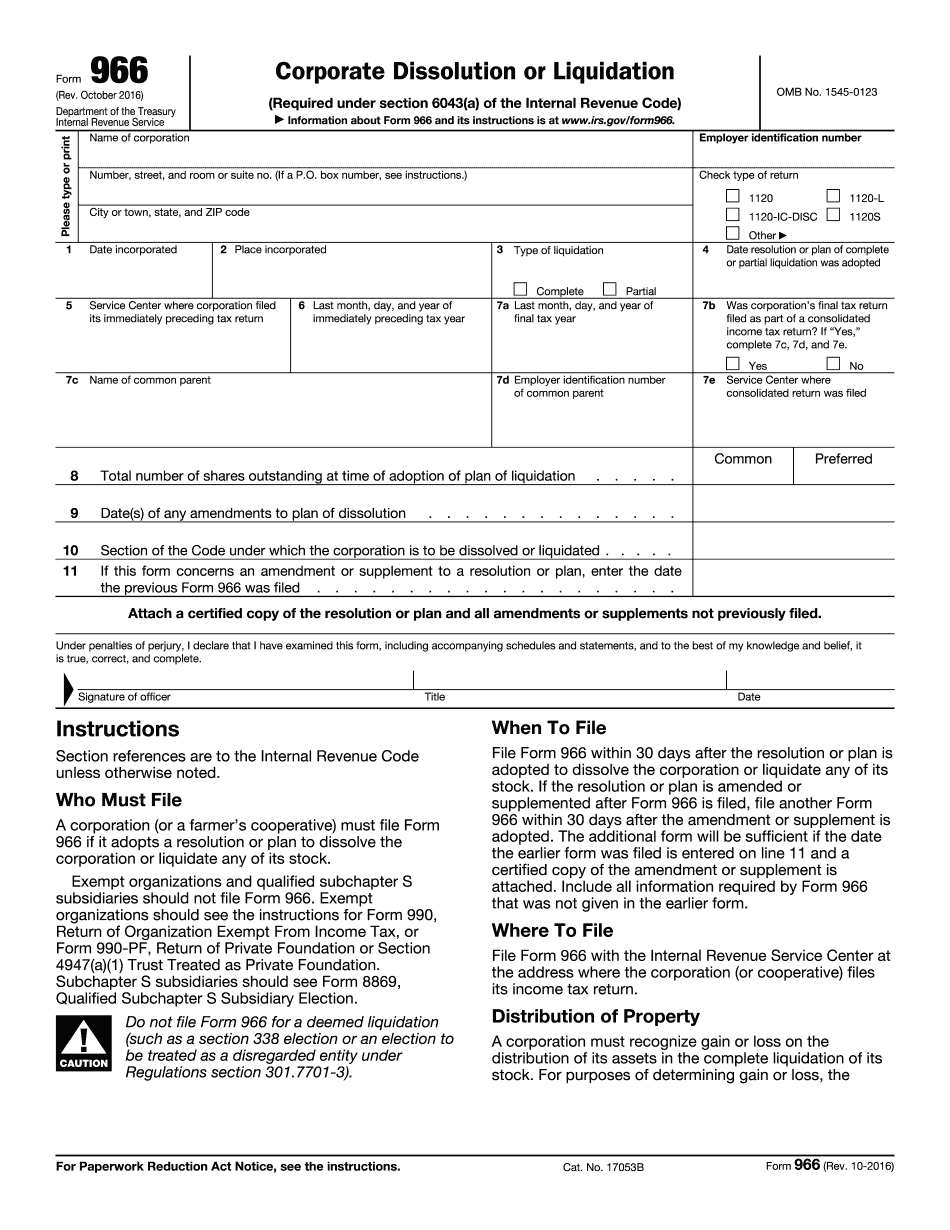

Tax consequences of dissolving an s corporation Form: What You Should Know

Mar 23, 2025 — The Internal Revenue Service (IRS) provides the specific guidance and instructions that corporations need to determine if an S corporation is subject to Section 954 and can continue to be operated. The form (Form 1 N) can be Sep 27, 2025 -- S corporation election for an S corporation that filed a petition to dissolve and file dissolution information Statement. S Corporation Disposition of Assets : The information for a dissolution proceeding and distribution of the corporation's assets is contained in the Form 1-5, Disposition of Personal Property of S Corporation. May 16, 2025 — The Tax Treatment of S Corporation Cash The S Corporation Income Tax and Gift Tax Information for Taxpayers Sep 16, 2025 — S Corporation Income Tax Information Publication, is a guide for taxpayers that may have a pending or expected case for dissolution of the S corporation. The guide includes the information provided in Form 1-5 but also explains information about dividends, interest and capital gain distributions and taxable distributions on the sale or exchange of securities. The guide also includes Form 1-8, Business Transactions and Guide to Taxable Distributions from an S Corporation. Forms: IRS Form 1040, U.S. Individual Income Tax Return, U.S. Business Tax Return (Individual Income Tax Return for Individuals), Individual Taxpayer Identification Number (ITIN) instructions for corporations and other taxpayers, and Form 941, U.S.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 966, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 966 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 966 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 966 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Tax consequences of dissolving an s corporation