Award-winning PDF software

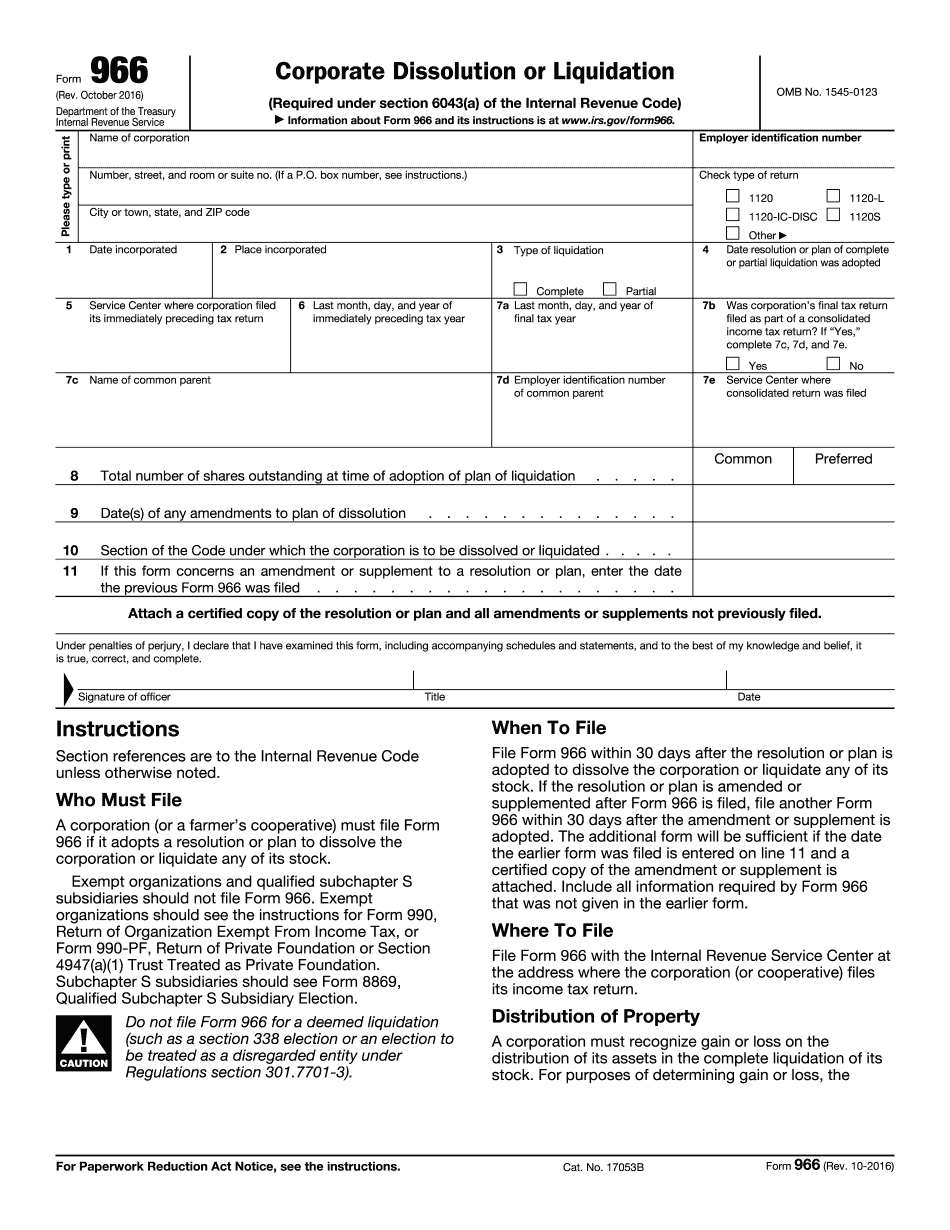

form 966 (rev. october 2016) - internal revenue service

If a corporation (or a farmer's cooperative) has more than one tax year and fails to file any of its returns on time (including a failure due to a failure to file a return to end a calendar quarter), it may be subject to penalty tax (in addition to interest imposed for the tax period). If a corporation (or a farmer's cooperative) has more than one tax year and fails to file its return for any year after the next fiscal year, it may be subject to penalty tax (in addition to interest imposed for the tax period). If either a corporation (or a farmer's cooperative) or the trustee (if any) has knowledge of the failure of a corporation (or a farmer's cooperative) to file its return for any fiscal year after the next fiscal year, the trustee may impose a penalty as punishment for the failure. If a corporation (or a.

About form 966, corporate dissolution or liquidation - internal

March 27, 2017 Form 966-S-EZ, Stock Split or Stock Acquisition, updated. February 6, 2017 Information about Form 966-S, Foreign Tax Credit, updated. December 29, 2016 Form 961-EZ, Current Report of Foreign Account (Netherlands) Income, updated. December 27, 2016 Information about Form 961, Statement of Foreign Bank and Financial Accounts, updated to include information relating to dispositions during 2016. April 28, 2016 Information about Form 966, Certificate of Election to Resign as a Shareholder, updated. January 15, 2016 Information about Share Capital Changes, updated. October 11, 2015 Information about Form 6198, Registration Rights Agreement for UAT, updated. To view form and terms of this agreement or inquire about its requirements, please visit the website. October 6, 2015 Information about Form 8885, Securities and Exchange Commission Form 20-F for Tax-Exempt Status, updated. August 30, 2015 Information about Form 991 information release, updated. August 17, 2015 Form 8-K, Registration Rights.

Form 966: (new) corporate dissolution & liquidation

Jul. 29, : “Form 966”. In-box: “Form 966”. Form 8863A. The Form 8863 is to be filed with the Secretary of State in the form prescribed by the Secretary of State. For more information on the Form 8863 and the instructions for filing, contact the Secretary of State at the toll-free number listed below. In-box: “Form 8863A”. In-box: “Form 8863A”. Form 709. The required Form 709 for corporations, or farmer's cooperatives, is required to be filed at the time of filing an election for dissolution, liquidation, succession or appointment of a special guardian. The corporate entity that has adopted a resolution or plan to dissolve and the trustee (or trustee's successor) of the trust must file such resolutions and plans with the Secretary of State along with (a) The election. A copy of the corporate entity's charter, bylaws and other instruments required or permitted by state laws.

form 966 (rev. december ) - reginfo.gov

If the corporation qualifies for tax exemption, this should list the organization as tax-exempt. If the corporation qualifies for tax exemption, this should list the organization as tax-exempt. Nonprofit organization. Check this box if you are a nonprofit organization that performs charitable services. This box if you are a nonprofit organization that performs charitable services. Qualified Domestic Relations Partner. Enter a statement on the following page that clarifies your relationship to your partner if you are not married. Enter a statement on the following page that clarifies your relationship to your partner if you are not married. Qualified Domestic Partner Name : Choose one, or select “Don't Know” to check all. Enter a statement on the following page that clarifies your relationship to your partner if you are not married. A list of items that must be in the “Employee's Last Name” box. Be sure this box is checked. A list of items.

Form 966 corporate dissolution or liquidation | upcounsel

For the debts and other liabilities of the corporation. S corporations are often used to buy a business. In order to be treated as an S corporation, all the shareholders must own 5% or more. If only the first 3 owners own 5% or more, the other 2 owners must own more than 10% if they are related to the first owner or the company. When the company's assets are sold, the IRS will make an “estimate” of the net assets of the company based on the percentage ownership. In this situation, many S corporations are left with only 2 people that own more than 20% of the assets of the company. If the 1st owner dies, who can assume the company ownership? If he or she did not provide the required 5% ownership, the assets could be sold, the business must be liquidated, and the assets distributed. The.