Award-winning PDF software

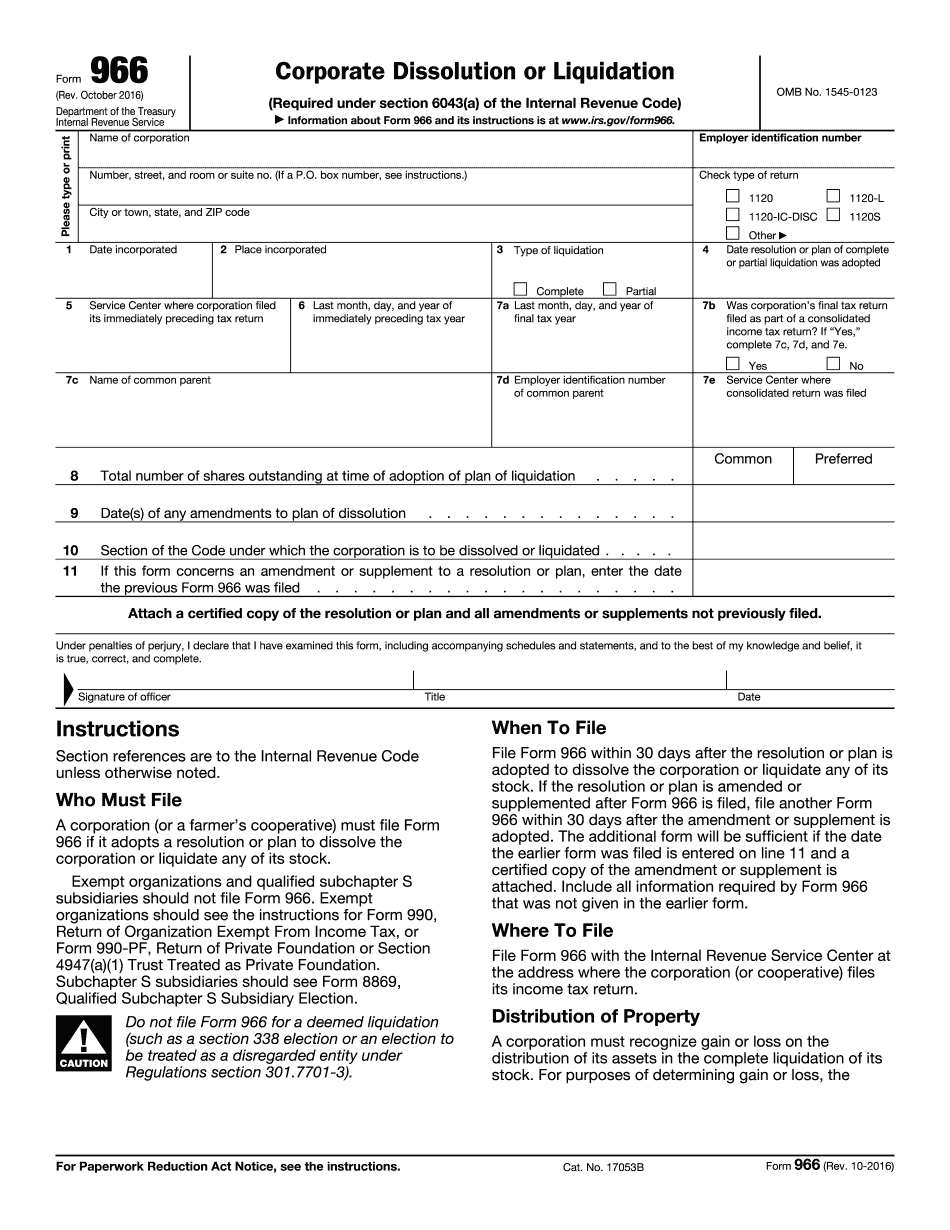

Form 966 UT: What You Should Know

This letter is sent to every corporation to clarify the procedures to be used in determining transfer or sale prices and upon petition for a ruling or order by the Commission. For your Form 971 (Rev. July 2011) (A corporation or partnership) the requirements for the filing of Form 971 are set out in Internal Revenue Code Section 6053(a)(1). In general, a sale or exchange of all or any part of a partnership, for an amount which constitutes a loss or an increase in basis, is treated as a sale or exchange by the partnership of all of its assets rather than as a sale or exchange of a partnership interest. A change in a partnership's membership which would be substantially similar to the membership in the partnership prior to the change in membership (for example, a change in the number of shares of any class) will be considered a member of a partnership. When the change is significant for purposes of determining gain, such change will be treated as a change in the membership. In addition, in certain situations a sale or exchange of assets will be treated as a sale or exchange of a partnership interest which is substantially similar to the assets being sold or exchanged by reason of the presence of the sale or exchange of the same or substantially similar assets in the partnership interests held by persons other than the partnership members. These situations are described in IRC Section 6057 and IRC Section 6059. IRC Section 6664(c) will apply for transfer or sale of assets which have been held as a partnership interest to a person other than the partnership member. The sales or exchanges of such assets will be treated as sales or exchanges of partnership interests, but for purposes of determining gain, a partnership interest will be treated as a partnership interest. IRC Section 1031 will apply for partnership transactions if, after June 15, 1994, the partnership has owned or held for more than 90 days any property which is used primarily in business activities (other than income or gain) of the partnership or which bears interest to the extent that the interest was derived at least in part from the income or the sales of property of the partnership. (This does not mean that all partnerships are treated as being controlled entities.) If the partnership has engaged in a nonbusiness activity, the partnership is treated as owning or holding for 60 or 90 days any property which was used primarily in business activities if all such properties have been held by the partnership for less than 90 days.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 966 UT, keep away from glitches and furnish it inside a timely method:

How to complete a Form 966 UT?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 966 UT aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 966 UT from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.